BONDS

Written by: on

Humphrey McQueen

Humphrey McQueen

The following is the text of Marxist historian Humphrey McQueen’s presentation on the Bond market and the capitalist economy from 3CR’s Solidarity Breafast program for 15 December 2018.

"My bond. I will have my bond."

Shylock, The Merchant of Venice, Act 3, sc. 3.

Shylock, The Merchant of Venice, Act 3, sc. 3.

Holidays are coming up – a time to venture into the new and the demanding. On this summer morning, we’re plunging into the global Bond market. It’s high time to shine a light on this corner of the endless economic upheavals.

‘Let them eat credit’

This is not the place to rehearse the history of either the bond market or the stock market. Suffice it to say that capitalism is built – in Marx’s phrase - on a ‘regime of credit’. As fixed-term loans, bonds are one part of that regime. Until the 1830s, most share-trading was in government bonds. (CONSOLS for Trollope aficionados.) What we now think of a stock market didn’t operate until the railway mania of the 1840s.

Why bother?

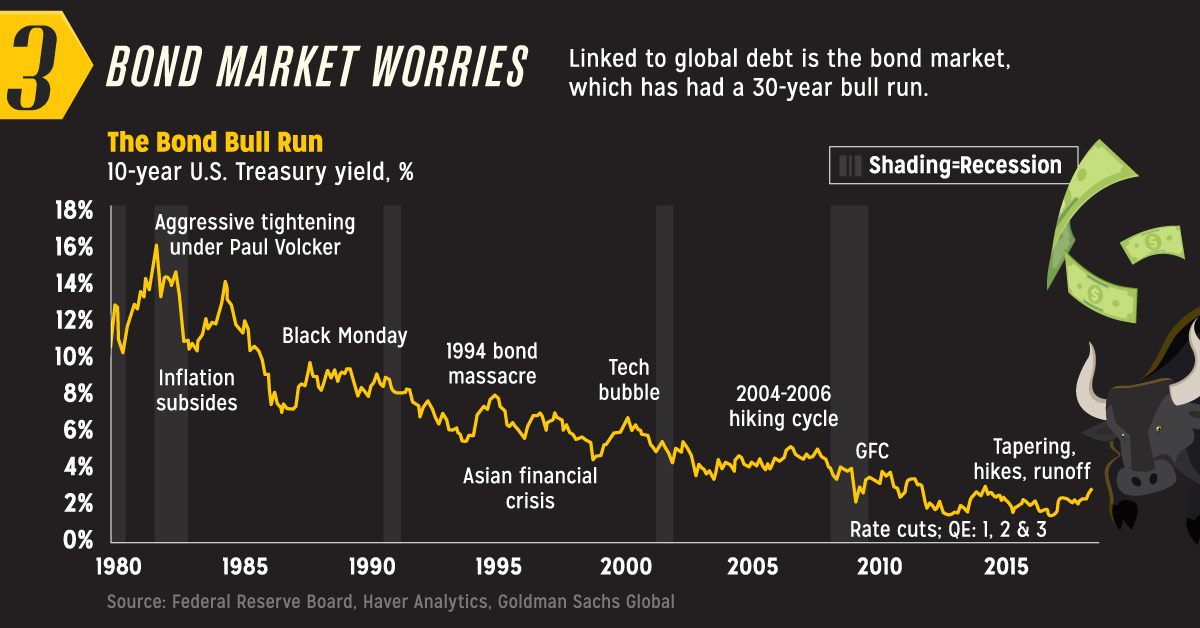

Several times a day the ABC delivers a stock-market report. In the evening, Alan Kohler tells us if ‘the market’ has had a bad-hair day. How often does the ABC so much as mention the Bond Market? Yet it’s more than twice the size of the share market: 100 trillion to 40 trillion. The stock-market’s a sideshow by comparison. Moreover, if bonds have a bad-hair day they can crash global share markets.

Stocks and bonds

Thanks to the screen jockeys, the kinds of bonds keep multiplying. In broad, there are government bonds and there are corporate bonds.

Let’s start from how a corporate bond differs from a share in that corporation. For once, the language of business comes close to the truth of the matter. If you buy a share you own a tiny slice in the firm. The promise is that you’ll get a share of the profit. Of course, if there’s no profit, you’ll get nothing.

A bond is quite different. It’s an IOU. After you ‘ve bought a corporate bond you still own only that bond. It gives you no part of the company and entitles you to none of its dividend. Instead, you’ve lent the company money for a fixed period and at a predetermined rate of interest.

No less importantly, you can expect to get paid that interest even if the company runs at a loss. Its interest payment is another business expense – like the power bill. So, income from a bond is regular and guaranteed. Moreover, if the firm does go bust, bondholders are high on the list of creditors to get their money back. By contrast, an ordinary shareholder is likely to lose the lot.

If you’re risk-averse, a bond is a safer bet than a share. That security comes at a cost. Across the past 250 years, the average interest rate offered on bonds has been lower than the average rate of profit on shares.

That average means that some bond issues must have offered rates better than share-price expectations. That’s as true for government bonds as for the corporates. Some of both are far riskier than others. Premium class are U.S. Treasuries.

Shorting Long-Term Capital

In 1997-8, Long-Term Capital Management came close to wrecking the system. The two founders had been given fake Nobel Prizes for concocting algorithms to smarten up the trades in derivatives. After the Asian crisis, these Masters of the Universe decided that US bonds were over-priced. They hedged accordingly.

Instead of US Treasuries falling, Russia defaulted on its bonds. That saw a panic sell-off of shares everywhere. Investors took fright, and then took wing to a safe asset. Hence, US Treasury Bonds went up – not down.

Long-Term Capital Management faced bankruptcy. The Federal Reserve corralled fifteen banks into putting up $3.5 billion. That rescue package saved the global economy from a meltdown like Lehman Brothers twenty years later.

Same difference in 2006. The current disruption began with the packaging of sub-prime mortgages into junk bonds.

Stimuls: QEs

After the 2008 implosion, the US Federal Reserve pumped money into the economy. The mechanism was to buy back government bonds. The Fed spent more than 8 trillion dollars in these Quantitative Easings. That’s $10,000 for every one on the planet. If you’re wondering whether your cheque is lost in the mail - it ain’t. It was delivered long ago to the financial institutions that manage wealth for the One Percent. That’s how the Uber-rich had got to own the Bonds that Treasury bought back. The flood of cash went to their merchant bankers and trust funds to re-invest.

Those firms were sitting on more capital than they could place at the average rate of profit. Trump’s tax cuts swelled this excess to pump the New York exchange to above 25,000 points.

Stock-market boom

Before the latest madness got started the deal was that you got $1 in dividend for every seventeen dollars you spent on a share. Now, you get $1 on every $30. The $1 return costs an extra $13. The price to earnings ratio, (or P:E.) used to be 17:1 - now it is 30:1.

Escalating entry-costs to the share-market coincided with the absence of new bond issues from safe governments. The safest bets were selling, not buying.

That conjuncture sent more than a few investors back to chasing junk bonds. Those issues offer much higher rates of interest. They must to attract funds into firms or for governments that carry a chance of going belly up.

Two to tango

This hunt for junk bonds airlifts us back two weeks to the recent G20 meeting in Buenos Aires. Almost a year ago we mentioned a truly remarkable event. The Argentinian government offered to sell $US17.75 billion in bonds. They won’t mature until the year 2117– yes, you heard right –100 years from now. Within two days, the offer had been over-subscribed. This rush to buy was just one more measure of how much excess capital is sloshing around.

There’s an even more remarkable aspect to the stampede of investors into Argentinian bonds. Buenos Aires has defaulted on international debts six times in the past 100 years. The most recent one was in 2014. You didn’t have to be Warren Buffett to predict what happened next.

Last August, Buenos Aires had to go to the IMF to borrow $US59 billion. The IMF bailout is bad news for the Argentinian workers. It imposed its usual regime of slashing welfare.

More generally, the fact that Argentina is still a member of the G20 - let alone the host nation for its 2018 summit - spotlights the mess that global capitalism is in twelve years after the sub-prime bond market began to fall apart in 2006.

If you missed out on lending to Argentina, don’t despair. There are plenty of other basket cases selling Bonds. In August last year, Iraq wanted to borrow one billion. It was swamped with offers of six. Argentina and Iraq don’t have a monopoly on junk bonds.

On one point, the experts agree: capitalism is in unchartered territory. It’s a mad, mad world.

Property as an ‘asset class’

What looks safer than a failed state?

The OECD has just warned about a hard landing for the Australian property market. What has that prospect got to do with the Bond Market?

Commercial property has long been an ‘asset class’ – like gold. Global wealth managers buy classes of assets. They are not buying this house or that apartment. The Melbourne boom was not powered just by individual Chinese bidding from the footpath.

The investors don’t know where these multi-million dwellings are.

Why should they? They never give a thought to living in them. They expect earnings from the rent and out of capital gains. Hence, the trigger for a property-market collapse could be when the wealth managers at Union Bank of Switzerland can find a better hole to hide in.

No, Teresa, there is no Santa Claus

Brexit offers a further round of Xmas cheer. The Pound is plunging. The Bank of England is buying corporate bonds to support the economy. How long before the Chancellor stops buying UK bonds to stimulate growth and starts selling them to prevent the collapse of Sterling, indeed, of the entire shebang?

Print Version - new window Email article

-----

Go back

Class Struggle and Socialism

Independence from Imperialism

People's Rights & Liberties

Community and Environment

Marxism Today

International

Independence from Imperialism

People's Rights & Liberties

Community and Environment

Marxism Today

International

Articles

| Drought |

| The Not-So Curious Incident of Low Wages Growth - Peetz report |

| Book Review: The Invisible Doctrine - The Secret History of Neoliberalism (& How it Came to Control Your Life) |

| Inflation hits Interest Rate Relief: The Crisis Grows! |

| Budget exposes myth of falling profitability and productivity |

| “Australian” companies that serve foreign capital |

| A suitable cause for alarm: what about the levers of power? |

| Profits - a system of economic crises, hardships and war |

| Book Review: Rent |

| Profits, Wages and Conditions |

| Bold Resistance grows to Corporates’ Economic Crisis and War |

| Agribusinesses Still Dominate Australia's Agriculture |

| Capitalism Develops and Expands in Ironic Ways |

| A bean-feast in the making: stimulus packages and the global economy |

| Climate change: Beware green swans with fat tails! |

| Uber |

| Marxism Today: The unfairness of a “fair day’s pay” |

| Reserve Army of Labour |

| BONDS |

| The relevance of Marx today |

-----